Systemic bankability is the key to unlocking energy transition speed and scale

About this paper

The pace of commercialization for emerging clean energy and industrial decarbonization technologies is insufficient to achieve ambitious climate goals. This is in part due to investment barriers that are largely unaddressed by existing analyses and policy frameworks. For emerging technologies, each project requires large amounts of capital to be at risk over multiple years in the face of considerable technological uncertainty and execution challenges. Such conditions do not align with the low-risk. profile sought by the large banks and infrastructure funds that finance large projects, nor does it align with the very high returns and short exit horizons sought by venture investors that finance tech start-ups. This mismatch is often referred to as the “missing middle,” that reflects the dearth of capital available for early deployment of infrastructure-heavy emerging technologies.

This paper, a collaboration between Clean Air Task Force, Princeton University’s Andlinger Center, and Mercator Partners, proposes a new framework: systemic bankability. Systemic bankability takes a systems view of the underlying conditions necessary and challenges holding back project finance for emerging net-zero technologies. The framework is intended as a methodical guide for policymakers, investors, technology start-ups, researchers and other stakeholders to identify key risks that act as investment barriers and to develop solution strategies that can unlock and accelerate deployment – starting with first of a kind projects and proceeding through the commercialization pathway to technology take-off.

Executive Summary

The pace of commercialization for emerging clean energy and industrial decarbonization technologies is insufficient to achieve ambitious climate goals. This is in part due to investment barriers and “chicken-and-egg” challenges that are largely unaddressed by existing analyses and policy frameworks. These challenges are especially acute for technologies characterized by capital-intensive infrastructure with long development lead times.

For emerging technologies, each first-of-a-kind and early-mover project requires large amounts of capital to be at risk over multiple years in the face of considerable technological uncertainty and execution challenges. Such conditions do not align with the low-risk profile sought by large project finance banks and private equity investors, or the very high returns and short exit horizons sought by venture investors. This mismatch, that is absent with “infrastructure-light” software and consumer technologies, is often referred to as the “missing middle”, reflecting the dearth of capital available for early deployment of infrastructure-heavy emerging technologies.

The missing middle is increasingly being recognized as a challenge but is typically depicted as the financing hurdles for first- to nth-of-a-kind projects. In reality, it can persist much longer, driven by a variety of policy, market, and industrial gaps rather than technology performance or cost.

The International Energy Agency (IEA) estimates that 75% percent of cumulative emissions reductions by 2050 will need to be drawn from technologies that are currently at the protype phase or not yet in mass market production1. Such technologies, including but not limited to low-emission fuels, advanced nuclear energy, next generation geothermal2, face a variety of investment obstacles that stifle their widescale deployment3. Continued delays in overcoming such challenges for nascent and new technologies are putting global decarbonization targets at risk.

To better inform how we tackle these challenges, we propose a new framework – systemic bankability. Systemic bankability takes a systems view of the underlying conditions necessary and challenges holding back project finance for emerging net-zero technologies. Its goal is to help policymakers, industry, and other stakeholders pinpoint policy, industrial, and business model gaps, and to develop solutions to unlock faster deployment speed and scale.

The Challenge of Financing New Clean Energy Technologies

Commercializing infrastructure technologies generally involves the progression from small-scale research and development (R&D) to widespread commercial-scale deployment. To bridge these end points, technologies need to deploy commercial-scale projects over time that improve the technology performance, reduce costs, and instill a high degree of confidence in investors that projects will deliver predictable returns.

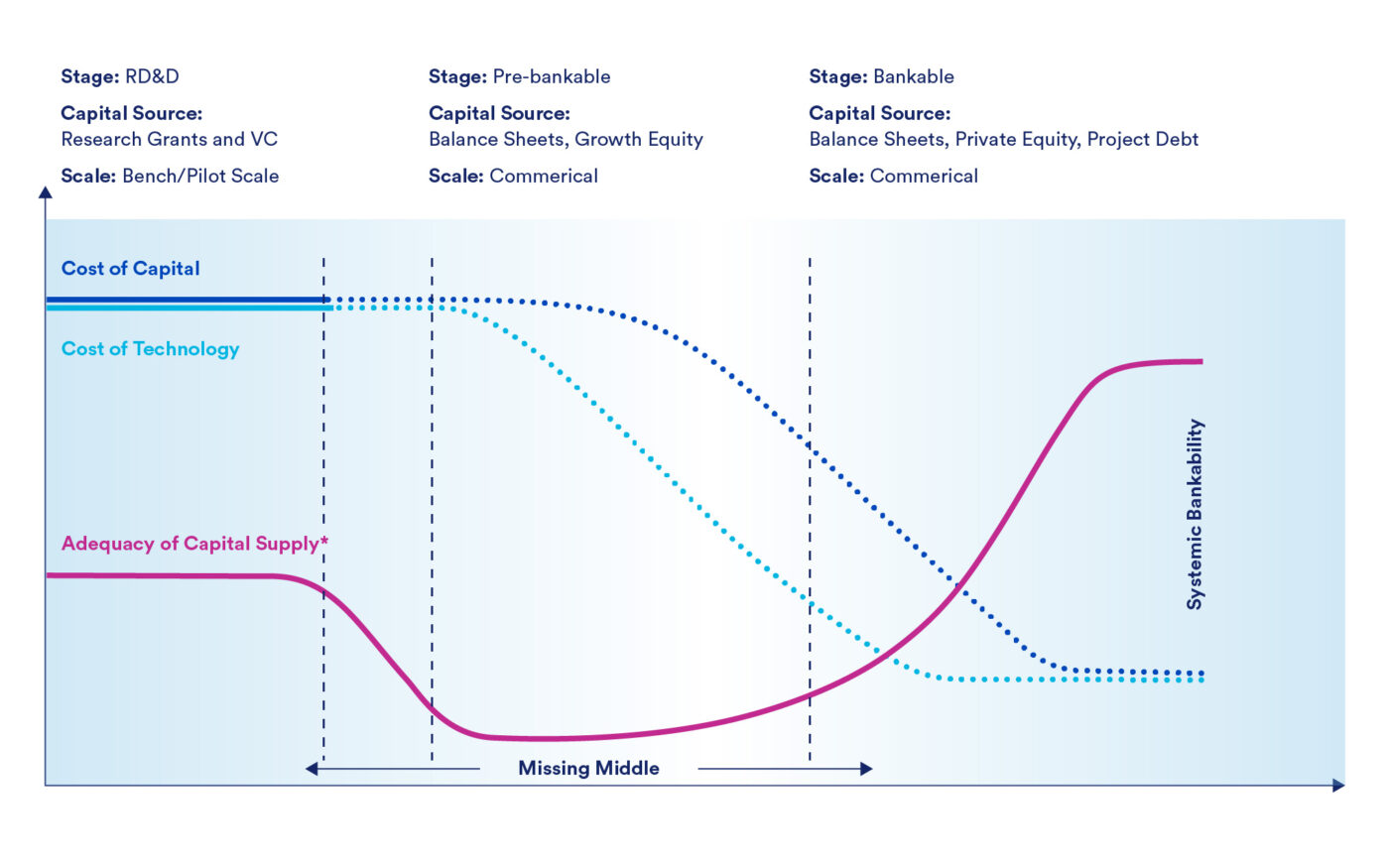

In practice, however, there is a structural investment gap referred to as the “missing middle” that delays or prevents the formation of this bridge4. Figure 1 characterizes the missing middle with stylized trajectories of the cost of capital, technology costs, and adequacy of capital availability through three stages of commercialization. On the left of Figure 1, modest investments in the R&D stage are risky because of the high potential for technological failure. A discrete pool of ‘venture’ investors and research grants place multiple bets with the goal of making outsized returns from at least one, in a short period of time. On the right of Figure 1, technology performance, competitiveness, and commercial viability are established. If returns are reliable and sufficient, projects are deemed “bankable” and can access a combination of low-cost equity and non- or limited-recourse commercial project debt5 6 to be deployed at a large scale.

Figure 1: Stylized illustration of typical evolution of cost of capital, adequacy of capital supply, and technology costs, and the “missing middle.”

In the middle section of Figure 1, however, there is a scarcity of investable capital that offers both infrastructure scale funding capacity and the risk tolerance to bridge this transition to large scale deployment. The scale of project investment at this point in the development of a technology, typically from $100 million to over a $1 billion, is generally too large for government research grants and venture capital. Meanwhile, the project risks are still too high for large institutional investors and commercial banks capable of providing infrastructure scale investment scale.3 4

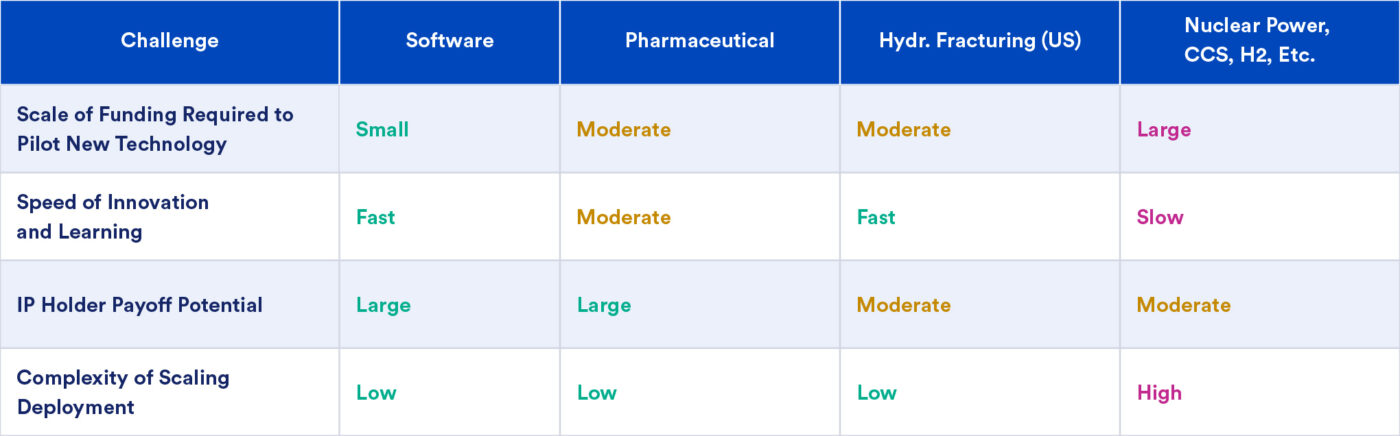

This “missing middle” underpins many challenges that are especially acute for energy and industrial production technologies but largely absent from more publicized software and consumer technologies. Google, for example, only needed to raise a modest $25 million before their initial success, becoming the commercial search engine for Yahoo, while Blackberry raised only $115 million in advance of their introduction of the world’s first smart phone.7 8 These ‘infrastructure-light’ technologies typically require less capital to advance pilots and demonstrations and face fewer system barriers to scaling deployment compared to infrastructure technologies. Figure 1 characterizes how the scale of the individual technology or project can exacerbate missing middle challenges.

Table 1: Energy Infrastructure Technology has Unique Challenges that Create Investment Market Gaps

Some of the challenges faced by these technologies are chicken-and-egg challenges. For example. electrolysis plants that produce green hydrogen need to be built to allow for price discovery in a yet to form market for low carbon hydrogen with unknow willingness to pay. Further, the full potential of cost reductions enabled by learning and scale will only be enabled by significant volume growth. Which comes first? This decision interdependency or “chicken-and-egg” dilemma also inhibits a credible investment case for new shared infrastructure networks that could accelerate scale-up and cost reductions, such as hydrogen pipelines and supply chains.9

Based on our collective experience and interviews with academic, policy, industry, and investor stakeholders, this concept of the “missing middle,”is broadly recognized by technology developers, energy and industrial companies, and private capital. However, these challenges are less well understood by policymakers and academic stakeholders who have the capacity to influence policies and other interventions to overcome these challenges.

For policymakers, existing frameworks like technology readiness level (TRL) only describe the status of technologies up to first of a kind projects. Frameworks such as the commercial readiness index (CRI) and adoption readiness level (ARL) serve as more robust tools for evaluating a technology’s development progress and competitive fit for potential markets.10 11 However, they are not targeted toward assessing the systemic risks to financing that prevail in the full “missing middle” commercialization pathway nor are they not designed to focus on identifying risk mitigation solutions. In academia, some business strategy research has focused on complex market ecosystem factors and technology adoption12 13 but that has typically not been a focus of clean tech commercialization literature. Meanwhile, nearly all deep decarbonization deployment models solve future pathways with perfect foresight and/or forced carbon reduction policies. These models often lack adequate representation of the financial system, and ignore the “missing middle,” chicken-and- egg interdependencies, and emergent challenges like social acceptance and lack of access to enabling infrastructure. 2 9

Because these existing frameworks and academic models are best suited for already commercialized technologies, they historically have inappropriately reinforced a narrow dual policy focus on (i) research, development and demonstration (RD&D) funding at early-stage bench-scale status, and (ii) production incentives (e.g. subsidies, tax credits, or avoided carbon taxes). More recently, existing frameworks have inspired government grants and loan guarantees as tools to support first-of-a-kind (FOAK) projects. While helpful for advancing early-stage technology development, as we discuss below, these do not fully bridge the “missing middle.”

Systemic Bankability Framework

This report introduces a new framework called systemic bankability to better characterize the conditions necessary to bridge the “missing middle.” We have identified nine risk factors that must be addressed to achieve systemic bankability and hence bridge the missing middle (see SI for descriptions):

- Risk Factor 1: Construction cost overrun risks

- Risk Factor 2: Technology performance risks

- Risk Factor 3: Revenue adequacy risks

- Risk Factor 4: Regulatory uncertainty

- Risk Factor 5: Enabling infrastructure networks (e.g. transmission) limitations

- Risk Factor 6: Social opposition

- Risk Factor 7: Supply chain limitations

- Risk Factor 8: Commercial insurance unavailability

- Risk Factor 9: Delivery system (e.g. workforce capacity, and engineering, procurement, and construction management (EPC) organizations) limitations.

While there are other risk factors that inform investment decisions, particularly before the missing-middle period, such as start-up management quality and capability as well the IP value of the technology, the nine risks outlined above relate to managing the missing middle risks and reaching systemic bankability.

Once these nine risk factors have been dealt with in a manner that is robust, widespread and durable for a technology or industry, systemic bankability is achieved which facilitates: i) access to abundant low-cost commercial capital to support large scale deployment; ii) credible asset sale options; and (iii) recycling of capital, where developers have the optionality to partially sell down or exit projects shortly after operational onset and reinvest in developing new projects, helping to drive speed and scale.

Individual commercial projects can sometimes bootstrap bespoke financing arrangements. This is in contrast to systemic bankability which represents the conditions required to underpin the predictable financial returns needed to mobilize large pools of low-cost private capital at the scale and speed of investment needed for mid- century net-zero goals. Systemic bankability does not simply materialize after the FOAK commercial project and may not even be achieved after the Nth of a kind (NOAK) project, unless all nine risk factors have been properly addressed.

Existing Gaps in Systemic Bankability Conditions

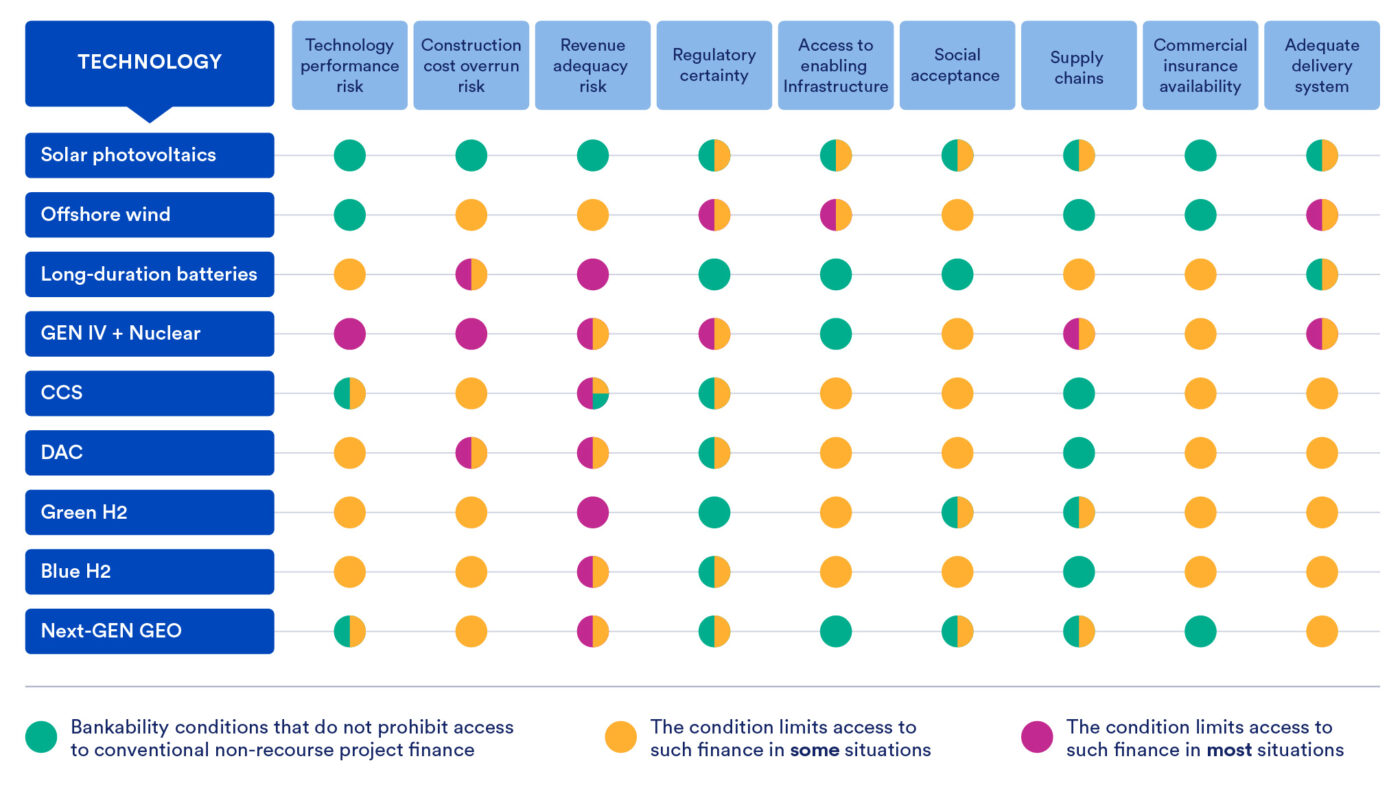

Figure 2 provides an illustrative high-level assessment of the current conditions relating to systemic bankability for different low carbon technologies. These risks may vary by market and this illustration is notionally based on conditions in the United States. Systemic bankability is achieved when all conditions are predominantly green. The existence of yellow and red conditions constrains a technology’s widespread deployment to various degrees. The coexistence of demand (market) and supply (technology) risks in particular, amplifies investor diffidence. The outcome from the application of this assessment will vary for a technology depending on specific circumstances, such as the sector application, policy and regulatory environment, and its geographical market.

Solar and onshore wind projects navigated the “missing middle” challenges and established systemic bankability over the last three decades with the support of a combination of large production subsidies, government procurement mandates that forced utilities to sign long-term contracts for production from projects, and access to pre-existing infrastructure networks. Combined with their modularity and relatively modest investment levels needed for early commercial scale projects, this enduring support also enabled the creation of robust supply chains, and deep project development capabilities. For example, solar PV commercialization enjoyed two decades of continuous generous incentives in the form of feed-in-tariffs, renewable energy certificates, and tax credits, but also benefited from (i) limited economies of scale allowing early commercialization projects of say 10 MW with a capital cost of just 10’s of millions of dollars; and (ii) existing transmission grid infrastructure enabling direct connection with end-use markets. Early progress encouraged growth and innovation in manufacturing to underpin a robust, low-cost supply chain, especially in China. In contrast, green hydrogen and carbon capture and storage have recently been granted subsidies, but economies of scale mean first-mover projects demand very large capital investments, and existing network infrastructure is virtually nonexistent.

Despite the impressive progress of wind and solar, conditions that were previously satisfied such as access to transmission infrastructure, supply chains, adequate workforce, and social acceptance have begun to bottleneck deployment.14 15 16 Processes to interconnect new electricity generation projects into transmission systems were not designed to handle the large numbers of renewable projects being developed today, local councils are blocking developments in response to community concerns, and geopolitical tensions have choked supply chains. As a result, new onshore wind deployment rates have slowed significantly both in the United States and Europe.17 This illustrates how systemic bankability, once achieved, is not permanently assured and can be eroded if not proactively maintained. The systemic bankability framework should therefore be used to anticipate and proactively address such risks on an on-going basis.

The multi-decadal timeline taken by solar and onshore wind to achieve systemic bankability was far too slow compared to the pace that emerging clean energy technologies will need if we are to achieve ambitious net-zero targets. The challenges in establishing systemic bankability conditions for some of these technologies will also be greater than for wind and solar. For example, advanced nuclear technologies, such as gaseous or thorium- based reactors, have high regulatory uncertainty (e.g. lack of advance design licenses) and nascent supply chain challenges (e.g. for new nuclear fuel types). For green hydrogen, high costs, limited electrolyzer performance history, lack of enabling infrastructure (e.g. hydrogen pipelines), and customers that do not have long-term offtake business models (e.g. refineries) present severe challenges.

Figure 2: Illustrative high-level illustration applying the systemic bankability conditions to clean energy technologies in the USA today relative to what is necessary to achieve net-zero by midcentury.

Note: this framework is not intended to describe the readiness for, or cost-effectiveness of any of the technologies in a particular application.

Using the Systemic Bankability Framework to Fill the Missing Middle

Investors, technology developers, researchers and policymakers can utilize the systemic bankability framework (SBF) to:

- Identify and prioritize risks that impact early-mover project viability and business value for early-stage investors;

- Help technology companies and investors better plan for, and organize around, addressing systemic risks; and

- Inform market and policy solutions to overcome critical barriers to investment and commercialization.

The framework can also be used to support a range of useful new support analyses, like scoring tools and systematic risk assessments. Such analyses must be adaptable over the full commercialization pathway from first through nth-of- a-kind, and ultimately to deployment rates at the speed and scale levels envisaged by ambitious climate goals.

Like the ARL and TRL, the SBF could be used to develop a numerical score as a snapshot of the status of specific technology areas and technology companies, thus providing a high-level comparator against other technology options. However, providing insights beyond high-level scores will be critical for understanding impacts of systemic risks, and developing strategies to address them, as well as facilitating more thorough examination of initial investment options.

To supplement decarbonization studies, researchers could assess practical systemic bankability risks and strategy gaps to better inform readers on the challenges ahead. For example, integrated assessment models (IAMs) and other climate models could characterize the magnitude of unmet investment needs driven by gaps and shortfalls in systemic bankability conditions and determine decarbonization shortfalls in the absence of additional policy. Then researchers and analysts could also explore the impact of mitigating those risks on accelerating investment and deployment.

Technology start-ups, early-stage investors, and project developers could use the framework to identify and rank the most significant risks along each stage of the commercialization path. This would help organize company and business strategies around risk mitigation priorities as they navigate the missing middle. For investors, the framework can help assess market valuation ranges and barriers to unlocking greater value.

For policymakers, the framework can help establish a thorough understanding of the drivers of systemic bankability gaps is necessary in order to develop an optimal mix of policies (Figure 3). For example, government grants and loan guarantees aiming to bridge the “missing middle” for FOAK projects, do little to address the predictability of permitting conditions, enabling infrastructure buildout, and other key systemic bankability conditions. Likewise, financial incentives, such as tax credits, can address cost premiums for projects, but this largely only benefits technologies that have already reduced other project risks.

Risks and mitigation strategies will change along development pathway, and the timing and shape of policy interventions must evolve in response. For example, for advanced nuclear and green hydrogen, most policy interventions should occur during emerging bankability to address early-stage technology risks, whereas for solar PV that has already achieved systemic bankability, policy interventions would more likely to be required to focus on maintaining or reestablishing enabling conditions to enable deployment at scale.

Figure 3: Non-exhaustive overview of policy actions that may improve certain bankability conditions for solar photovoltaics, advanced nuclear, and green hydrogen.

Ultimately, no single strategy will be the solution and an integrated approach is necessary. In some cases, technologies will need bespoke strategies to address certain risks and in other cases the same strategy can address a similar risk across a range of technologies. Applying the SBF from various perspectives across the range of potential solutions will help inform early-stage technology investment choices, commercialization strategies, and the evolving suite of policies to maximize value over time.

Conclusion

To achieve systemic bankability and overcome the investment “missing middle”, stakeholders will need to identify gaps in systemic conditions by technology, industry, and jurisdiction; characterize specific policies to address gaps; understand and execute the optimal timing of policy actions; and develop coordination mechanisms across institutions, to address all potential gaps across a technology. The systemic bankability framework, presented here, is one framework that can help identify the needs and solutions. Our hope is that investors lenders, technology start-ups, and policymakers will use this framework, or something similar, for that purpose.

Footnotes

- IEA (2020), Energy Technology Perspectives: Special Report on Clean Energy Innovation Accelerating technology progress for a sustainable future, IEA, Paris https://www.iea.org/reports/clean-energy-innovation.

- IEA (2021). Net Zero by 2050: A Roadmap for the Global Energy Sector. IEA, Paris https://www.iea.org/reports/net-zero-by-2050.

- Mazzucato, M., and Semieniuk, G. (2018). Financing renewable energy: Who is financing what and why it matters. Technol. Forecast. Soc. Change 127, 8–22. https://doi.org/10.1016/j.techfore.2017.05.021.

- A. Arora, A. Fosfuri, & T. Rønde, “The missing middle: Value capture in the market for startups.” Research Policy, 2024. https://doi.org/10.1016/j.respol.2024.104958

- C. Greig, et al. “Speeding up risk capital allocation to deliver net-zero ambitions.” Joule, 2023. https://doi.org/10.1016/j.joule.2023.01.003

- D. Reicher et al. “Derisking Decarbonization: Making Green Energy Investments Blue Chip.” https://law.stanford.edu/wp-content/ uploads/2017/11/stanfordcleanenergyfinanceframingdoc10-31_final.pdf

- Google press release, June 7, 1999. https://googlepress.blogspot.com/1999/06/google-receives-25-million-in-equity.html?

- “Timeline: Change at the Top of Reseaerch in Motion”, Reuters, September 30, 2022. https://www.reuters.com/article/markets/timeline- change-at-the-top-of-research-in-motion-idUSTRE80M051/

- S. Uden, et al. “Bridging capital discipline and energy scenarios.” Energy & Environmental Science 2022, 15, 3114. https://doi.org/10.1039/d2ee01244h

- Government of Australia. “Commercial Readiness Index for Renewable Energy Sectors.” 2014. https://arena.gov.au/assets/2014/02/ Commercial-Readiness-Index.pdf

- U.S. Department of Energy. “Commercial Adoption Readiness Assessment Tool (CARAT).” 2023. https://www.energy.gov/sites/default/ files/2023-03/Commercial%20Adoption%20Readiness%20Assessment%20Tool%20%28CARAT%29_030323.pdf

- R. Adner, K. Rhul. “Innovation ecosystems and the pace of substitution: Re-examining technology S-curves.” Strategic Management Journal 2015, Volume 37, 4. https://sms.onlinelibrary.wiley.com/doi/abs/10.1002/smj.2363

- A. Miller, et al. “Nested barriers to low-carbon infrastructure.” Nature Climate Change 2016, 6, 1065-1077. https://www.nature.com/articles/nclimate3142

- BloombergNEF. “A Power Grid Long Enough to Reach the Sun Is Key to the Climate Fight.” 2023. https://about.bnef.com/blog/a-power-grid-long-enough-to-reach-the-sun-is-key-to-the-climate-fight/

- R. Nilson, et al. “Halfway up the ladder: Developer practices and perspectives on community engagement for utility-scale renewable energy in the United States.” Energy Research & Social Science 2024, 117. DOI: 10.1016/j.erss.2024.103706.

- B. McDowell, et al. “National Wind Energy Workforce Assessment: Challenges, Opportunities, and Future Needs.” 2024. NREL. https://www.nrel.gov/docs/fy24osti/87670.pdf

- Clean Investment Monitor. “Clean Investment in 2023: Assessing Progress in Electricity and Transport.” 2024. https://cdn.prod.website-files. com/64e31ae6c5fd44b10ff405a7/65d568670df0b04daed42371_Clean%20Investment%20in%202023%20-%20Assessing%20Progress%20 in%20Electricity%20and%20Transport.pdf

Appendix

A1. Description of Bankability Conditions

- Access to commercial insurance: Whether the project can access commercial insurance to insure its financial performance.Construction Cost Overrun risk: The risk that the construction costs projected at the time of final investment decision get significantly inflated during the construction period.

- Technology Performance Risks: Risks related to the technology or overall project not performing as expected at FID, which includes lesser output than expected or higher operating costs than expected.

- Revenue adequacy risk (volume and price) Risks: Risks related to whether the project will earn the necessary amount of revenue to satisfy financial obligations.

- Regulatory certainty: Risks related to the predictability and efficient implementation of policies relevant for the financial performance of the project, including permitting complexity and timelines.

- Access to enabling infrastructure networks: Whether a project can access the necessary infrastructure networks for its operations and performance. Such networks may be electricity transmission, fuel pipelines, carbon dioxide pipelines and storage, and others.

- Social acceptance: Refers to the social license to locate and operate a project within its community.

- Robust supply chains: Refers to the robustness of the supply chains necessary to build and operate a project.

- Adequate delivery system: Refers to whether there is enough labor to build and operate a project. Examples include financial deal processing capacity, and engineering, procurement, and construction management, and skilled operating labor.

When these conditions are met, project financing capacity is typically available and specific project investment risk is limited to judgments about project configuration, quality of feasibility studies, and the track record of the proponents. Conversely, pre-bankable projects lack some or all of these conditions, making them riskier, limiting the pools of capital willing to invest, and ultimately making them difficult, and more expensive, to finance. Without adequate conditions, many struggle to secure even the initial development capital needed to reach a Final Investment Decision (FID). In limited circumstances, project financing of a limited amount of commercial-scale demonstrations of an early-stage technology may still be possible under bespoke combinations of incentives, contracts, and guarantees. Often, such projects must be financed on the balance sheets of large companies, who have capacity to absorb a limited number of underperforming or failed projects

Credits

- Kasparas Spokas, Clean Air Task Force

- Darryle Ulama, Clean Air Task Force

- Chris Greig, Princeton University

- Kurt Waltzer, Energy Systems Innovation Consulting

- Scott Hobart, Mercator Partners